Why Mortgage Calculators Fall Short

Why Speaking With a Loan Officer First Can Save You From Costly Surprises

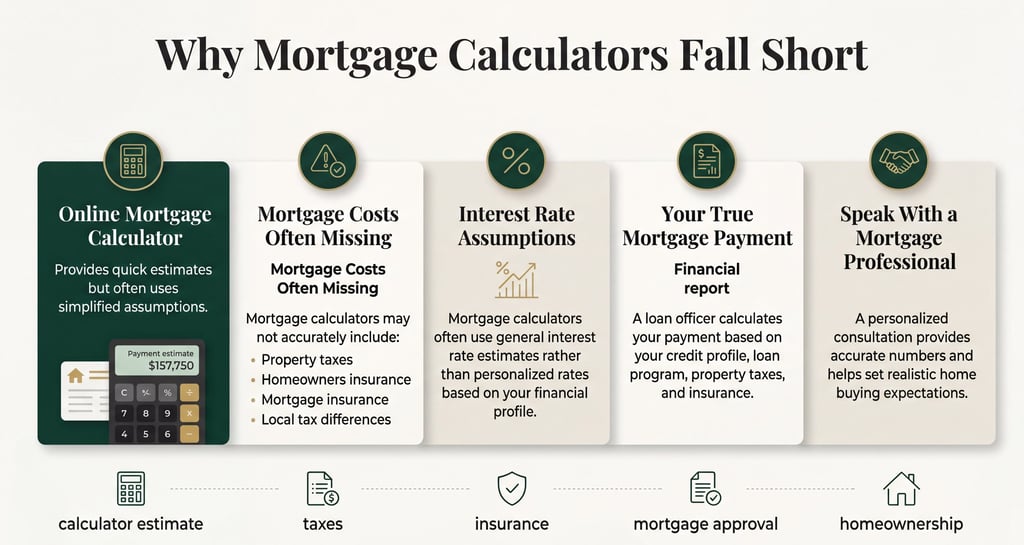

Why Online Mortgage Calculators Are Often Inaccurate

And Why Speaking With a Loan Officer First Can Save You From Costly Surprises

If you're thinking about buying a home, one of the first tools you may turn to is an online mortgage calculator.

Mortgage calculators are extremely common and can be useful for rough estimates, but they often fail to reflect the true cost of homeownership.

Many buyers begin their home search based on these numbers, only to discover later that their actual mortgage payment is very different.

Setting the correct expectations early in the home buying process is one of the most important things you can do to avoid frustration later.

Let’s break down why mortgage calculators frequently fall short and what you should do instead.

Are Mortgage Calculators Accurate?

The short answer is not always.

Mortgage calculators typically rely on simplified assumptions and generic data inputs. While they can provide a basic estimate, they often fail to account for several important factors that influence your actual monthly mortgage payment.

These tools typically calculate only:

Purchase price

Down payment

Interest rate

Loan term

However, a true mortgage payment often includes many additional costs that calculators do not estimate correctly.

What Mortgage Calculators Often Get Wrong

When borrowers search online for “how much house can I afford” or “mortgage payment calculator,” they are often shown simplified estimates that don't reflect the full financial picture.

Here are some of the biggest reasons these estimates can be inaccurate.

Property Taxes Are Frequently Estimated Incorrectly

Property taxes vary significantly depending on:

City or county

Local tax rates

Property assessments

Changes in tax laws

Many online calculators use national averages or outdated tax data, which can make payment estimates inaccurate.

For example, if property taxes are underestimated, a calculator might show a monthly payment that is hundreds of dollars lower than reality.

An experienced loan officer reviews the actual property tax structure for the specific area you are buying in.

Homeowners Insurance Is Often Underestimated

Mortgage calculators frequently use simplified assumptions when estimating homeowners insurance.

However, insurance costs vary depending on:

Property value

Location

Insurance provider

Coverage requirements

Risk zones such as flood areas

Without these details, calculators often provide estimates that do not match real insurance premiums.

Mortgage Insurance May Not Be Included

Depending on the loan program you choose, your payment may include mortgage insurance, which calculators often fail to include properly.

For example:

FHA Loans

Include both upfront mortgage insurance and monthly mortgage insurance premiums.

Conventional Loans

May require Private Mortgage Insurance (PMI) depending on the down payment.

VA Loans

Include a funding fee that can impact your loan structure.

Each program has unique guidelines, which is why generic calculators struggle to provide accurate estimates.

Interest Rates Change Frequently

Mortgage interest rates move daily and sometimes multiple times throughout the day depending on market conditions.

Many calculators assume a static interest rate, which may not reflect current market pricing.

Your interest rate depends on several factors including:

Credit score

Loan program

Down payment

Loan size

Market conditions

This is why two borrowers purchasing similar homes may receive different mortgage rates.

Why Incorrect Estimates Can Create Problems During the Home Search

When buyers start their home search based on unrealistic payment estimates, it can lead to frustration later.

For example:

A mortgage calculator might estimate a payment of $2,500 per month.

However, after accounting for taxes, insurance, and mortgage insurance, the true payment could be closer to $2,900 per month.

That difference can change:

Your home search price range

Your monthly affordability

Your financial comfort level

Your DTI Ratios in which an increase here could negatively impact your qualifying factors

Starting with accurate numbers helps avoid this situation.

Why Speaking With a Loan Officer First Is the Best Approach

Instead of relying solely on mortgage calculators, speaking with an experienced loan officer can provide a much clearer picture of what your true mortgage payment may look like.

A professional mortgage consultation evaluates factors such as:

Credit profile

Income structure

Debt-to-income ratio

Loan program eligibility

Property tax estimates

Insurance costs

Current mortgage interest rates

This creates a customized payment estimate based on real numbers, not generic assumptions.

Setting the Right Expectations From the Beginning

Buying a home should feel exciting and empowering, not confusing or stressful.

When you begin the process with clear financial expectations, you can focus on finding the right home rather than adjusting your plans later.

Accurate planning makes the home buying journey smoother for everyone involved.

Speak With a Mortgage Professional Before Relying on Online Calculators

If you are considering purchasing a home in Virginia, Maryland, or Washington DC, having an experienced mortgage professional guide you through the numbers can make a significant difference.

At Aurelium Home Loans, I offer no-obligation consultations where we review your financial goals and discuss what your potential mortgage payment may look like based on real data.

You are always welcome to reach out with questions.

Want to Know What Your Real Mortgage Payment Could Be?

Schedule a conversation and receive a personalized estimate based on your financial profile and current market conditions.

- Jake Bumbrey Jr-

Licensed MLO: NMLS #2603530 (VA)

Get In Touch

8401 Mayland Dr #6807

Richmond, VA 23294

Office Hours: Daily 9am-9pm ET

© 2026 Aurelium Home Loans. All rights reserved.

Powered by: